,allowExpansion)

The digital future of financial assets

In the Financial Services industry, an important opportunity enabled by blockchain is Digital Assets, which are becoming increasingly popular in global markets.

Financial assets: key figures

In the Financial Services industry, an important opportunity enabled by blockchain is Digital Assets, which are becoming increasingly popular in global markets, as can be seen in the figures involved.

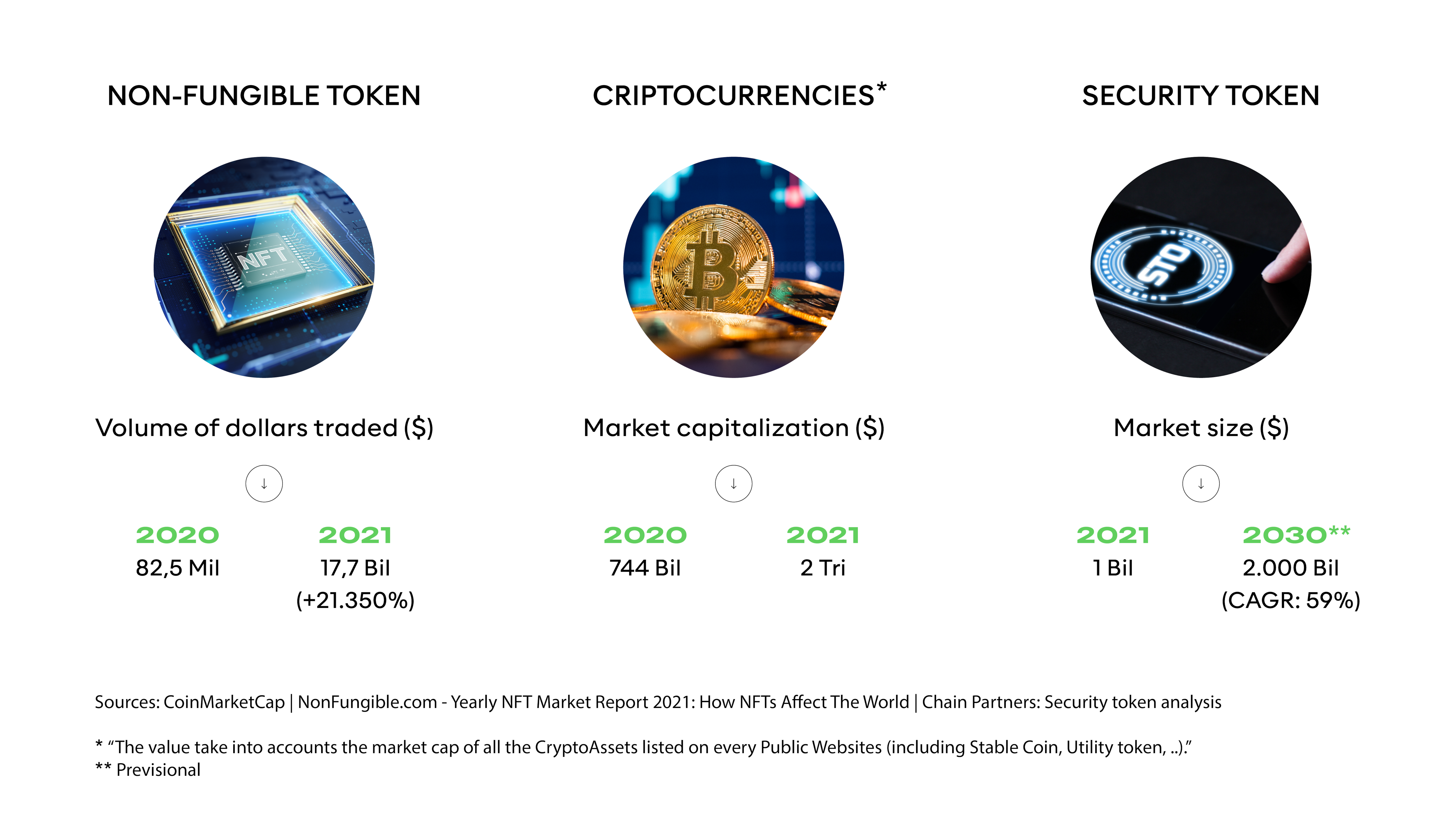

In terms of prominence, payment tokens are without doubt the most mature of the developments concerned, with cryptocurrency investments worth as much as $2 trillion in 2021. These are followed by NFTs, the use of which has expanded dramatically over recent years. The value of NFT transactions grew from $80 million in 2020 to over $17 billion in 2021. Security tokens, however, are the newest form of digital asset. It is estimated that their market value, subject to the necessary regulatory developments, will exceed $2,000 billion by 2030.

Figure: Market trends for cryptocurrencies, NFTs and security tokens

NFTs and security tokens are undoubtedly a rapidly growing phenomenon and are attracting increasing investor attention. Relative to the financial market overall, however, they do not yet represent a major area of investment compared to traditional instruments.

Financial assets: opportunities for banks

While NFTs and security tokens still occupy a niche position within the overall market, the growing interest from business and the benefits of blockchain technology make these new products an attractive opportunity for Financial Services operators.

Faced with these changes and the overall evolution of the sector, banks have no choice but to react, and should leverage digital assets in two areas:

Technology: by exploiting the advantages of blockchain to streamline their product creation and management processes

Business: by expanding their commercial offering with new products and services.

The combination of these two aspects (technology and business) can bring benefits for banks in terms of:

Attracting young customers: millennials and members of Generation Z are highly interested in the digital asset market and the metaverse. By integrating products and services related to this ecosystem, banks can attract and retain a market segment that is typically not fully served but is of major importance for future growth and generational transitions;

Internationalisation: in an increasingly competitive and rapidly growing market, opening up to digital assets enables banks to strengthen their international position by accessing a market that, thanks to the technology involved, is truly global;

Investment affordability: blockchain allows financial instruments to be subdivided and lowers the minimum threshold for accessing the investment market; for banks, this expands the pool of potential customers, by giving to those with a lower spending capacity access to products currently reserved for high-net-worth and institutional investors;

Diversification: digital assets represent a new asset class to invest in and they can help diversify a bank’s portfolio, making it more attractive for its customers;

Automation: the automation brought by blockchain technology enables banks to streamline the operational processes involved in managing and trading financial instruments.

The financial investment market

From a commercial perspective, the main types of services that banks can integrate using digital assets consist of:

Wallets: a storage service for digital assets that can potentially be integrated within a bank’s traditional home banking system to offer customers an alternative and secure tool for managing their transactions in the metaverse and in the digital asset ecosystem generally. If we think of banks as offering the gold standard of payment systems, the wallet can be seen as a new payment method linked to a person’s bank account – one that, like a credit/debit card, allows operations in the virtual world and potentially in the real world as we currently know it.

Exchange & trading: financial operators will be able to facilitate the exchange of traditional currency for virtual currency and, via trading solutions, enable the purchase and sale of digital assets by allowing customers to exchange, for example, a bitcoin for a security token rather than an NFT. By integrating this service, banks can position themselves in a market that is of certain interest to their customers and avoid, in the long term, a large-scale loss of custom and therefore revenue.

Financial advice: in other words, a holistic financial advice model that also takes into account the customer’s digital asset base. Large financial industry players will be able to develop new distribution models by leveraging their skills and levels of digitisation while potentially delineating increasingly sophisticated service levels, such as:

A first level, typically more “mass market” in nature, aimed at providing general advice on digital assets, by creating a comprehensive view of the customer’s financial portfolio and diversifying traditional investments with cryptocurrencies, security tokens and so forth.

A second level of “specialist advice”, which analyses the factors underpinning digital asset investments by providing customers with specific guidance based on their requirements and preferences, and taking into account their attitude to risk. This service can also be provided via third-party partners that specialise in the underlying investments.

Wallet

)

Exchange & Trading

)

Financial Advisory

Impacts of digital financial assets on the value chain

To enrich their commercial offering with these new services, banks will need to take action with regard to their value chain in terms of both building new expertise in the management of digital assets and in developing their IT systems with the aid of blockchain-based platforms and applications. As always, the integration of new technologies involves two possible strategies (“make or buy”):

the formation of partnerships with new specialist operators / challenger banks that already offer these services;

in-house development of all the components necessary for providing the services concerned (such as a wallet service and/or trading / exchange platform).

During the initial phase of the market, it is essential that partnerships are developed with players specialising in digital assets to ensure rapid positioning on the market. This strategy will not only enable a faster time-to-market - i.e by developing the service and modifying it in response to regulatory changes - but will also enable banks to gain the necessary expertise. A strategy for internalising certain components can also be assessed from a long-term perspective, where the key to success will involve differentiating a bank’s services from those of its competitors.

The regulator’s role for the financial services market

In this dynamic and fast-growing environment, a key role will be played by the regulator, which needs to maintain protection for investors and market stability while also encouraging innovation in the sector.

The European regulator is already working on rules governing the issuing and distribution of digital assets. The main ones are the:

Markets in Crypto Assets (MiCA) Regulation: this is a European Commission regulation that applies to crypto assets not qualifying as financial instruments and aims to establish a clear and uniform framework for digital finance;

Pilot regime (Regulation (EU) 2022/858): this is aimed at supporting the process of developing the secondary crypto business market and the adoption of DLT – Distributed Ledger Technology in the trading and post-trading areas - e.g. systems based on a distributed ledger such as blockchain.

The opportunities created by digital assets, combined with a push by regulators and the new processes enabled by blockchain, have the potential to profoundly transform the financial services market.