SOT – Recalibration of shocks for IRRBB

SOT - High-level recap

The Supervisory Outlier Test (SOT) is a regulatory tool used to scrutinize banks’ exposure to interest-rate risk in the banking book (IRRBB). Under the SOT banks must simulate a set of prescribed interest-rate shock scenarios and assess the impact on two primary metrics:

· Economic Value of Equity (EVE) — the present value change of banking-book cashflows under the shock.

· Net Interest Income (NII) — the change in expected one-year interest income (minus expense) under a constant-balance-sheet assumption.

These measures give supervisors insight into both the long-term and short-term effects of rate movements on a bank’s balance sheet. If the imposed shocks result in losses beyond defined thresholds, such as an EVE decline greater than 15% of Tier 1 capital (based on the 6 defined scenarios) or an NII decline above 5% (based on the 2 parallel scenarios), the bank is flagged as an “outlier.” This does not automatically trigger capital penalties but prompts supervisory dialogue under the Supervisory Review and Evaluation Process (SREP).

Introduction

The interest-rate environment has changed significantly over the past decade. Following a long period of low if not negative rates, many central banks engaged in aggressive policies in the course of 2022 by significantly raising interest rates in a context of surging inflation. The subsequent normalisation cycle, which was characterised by a prolonged period of an inverted yield curve, led to a stabilisation of interest rates at levels markedly higher than what prevailed previously.

Regulators have not remained inactive and intensified their oversight of banks’ IRRBB management frameworks (e.g., the EBA 'heatmap', the multiplication of ECB on-site inspections and targeted reviews). Indeed, while the shift in the interest rate paradigm has significantly boosted profitability, it has also introduced new risk management challenges driven by heightened market fluctuations and less predictable client behaviors.

In that context, The Basel Committee has also proposed to re-calibrate the shocks used in the SOT, to ensure those reflect current and expected rate volatility. These updates address weaknesses in the old methodology, which struggled to capture movements when rates were near zero.

Overview of the new shocks and methodological changes

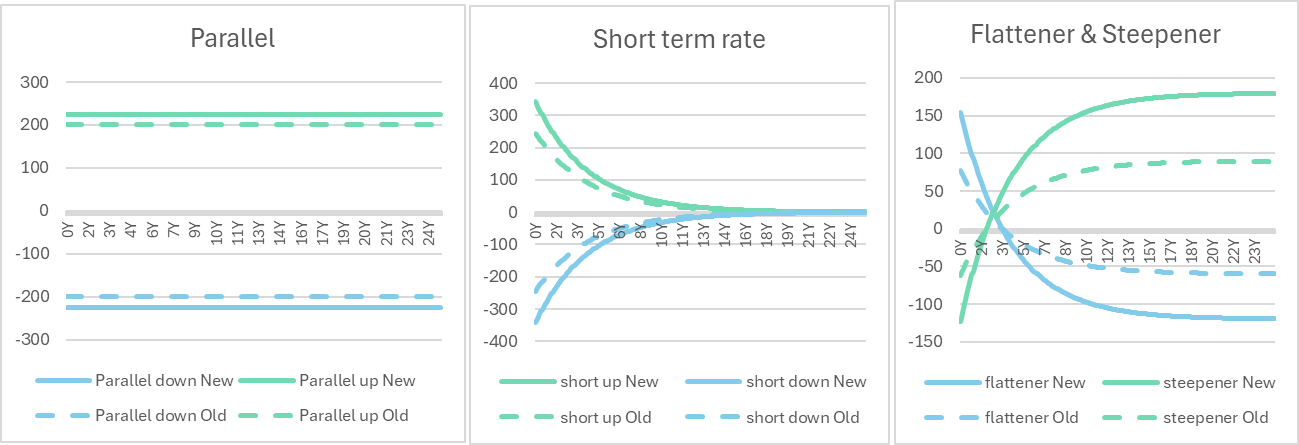

The revised SOT framework keeps the same six standard shock scenarios but updates their amplitudes to reflect recent market conditions. More specifically, the calibration dataset now covers data up to end-2023, reflecting both the earlier low-rate environment and the significant rate hikes of 2022–2023. The recalibration also introduces locally derived shock factors for each currency, increases the confidence level from the 99th to the 99.9th percentile and refines shock rounding from 50 to 25 basis points.

As a result, parallel up and down shocks are now slightly larger, and the steepener and flattener scenarios are more pronounced as illustrated below.

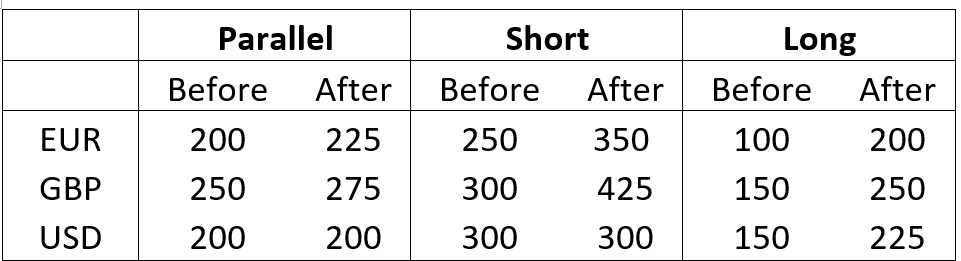

An overview of the shocks for the main currencies is provided in the table below, highlighting that EUR and GBP are the most affected by the revisions.

Implications for banks

For banks, the recalibration of shocks is relatively straightforward to implement and should not pose major operational challenges. However, the resulting implications for interest rate risk management can be significant. Measures of IRRBB will rise without structural changes to the balance sheet, while at the same time the reform does not include a review of the defined thresholds to be designated as ‘outlier’. To avoid greater supervisory scrutiny, banks will therefore need to reassess their risk appetite and internal limits to ensure adequate buffers under the revised calibration.

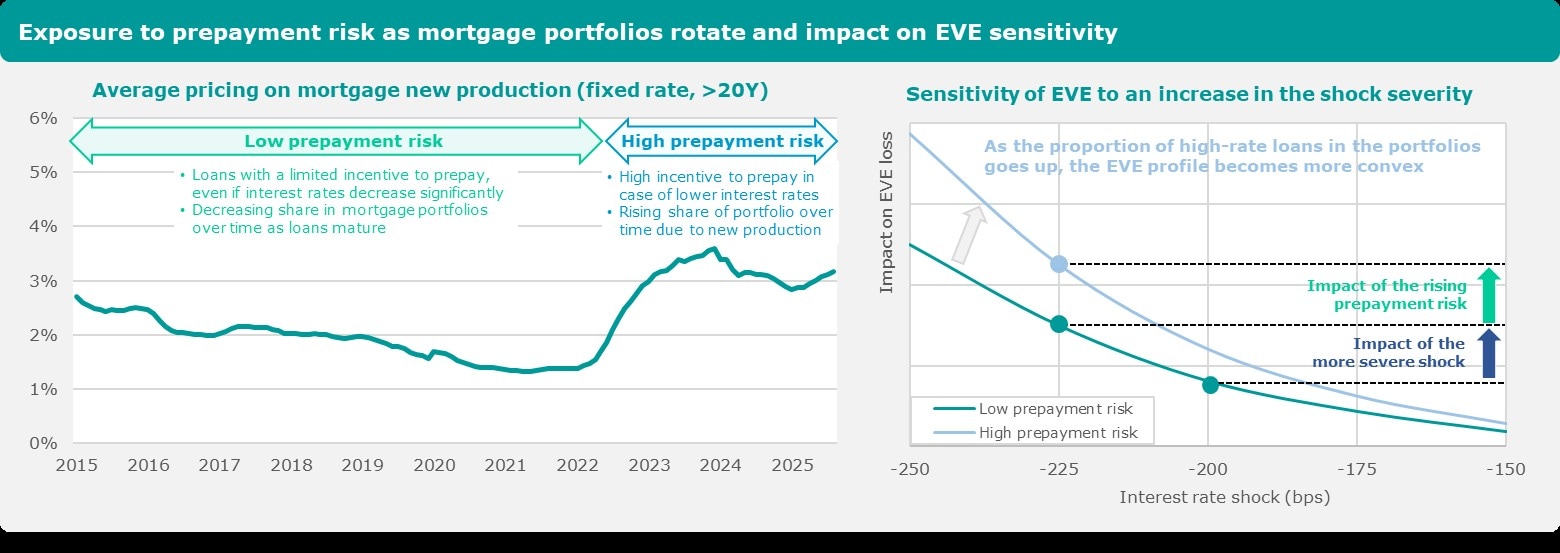

Additionally, the impact of this recalibration on SOT outcomes should not be under-estimated. Indeed, even modest increases in parallel shocks can produce disproportionately larger EVE losses because of convexity effects. This sensitivity is particularly pronounced for institutions with large portfolios of fixed-rate loans originated at high interest rates. When rates decline, prepayments may accelerate, reducing the stock of high-yielding assets and compressing margins.

In that respect, the timing of the review of the SOT scenarios coincides with an increase in exposure to prepayment risk as the stock of high-rate loans builds up, creating potential for refinancing in case of lower market rates. Indeed, low-rate loans originated before 2022 are gradually replaced by new mortgages at higher rates – which will increase the levels of prepayments expected under the downwards interest rate shocks.

The mechanism is illustrated below:

Hedging practices may need to be revised as traditional interest rate swaps that are ill-equipped to address such option risks. Instruments such as swaptions, caps, and floors are likely to play a greater role in managing convexity, supporting a more adaptive and resilient interest rate risk management framework.

Another potential consequence of the recalibration is to alter the hierarchy of the most impactful scenarios. Currently, the parallel shocks typically represent the most severe impacts on EVE for most banks but this may change as the steepener and flattener scenarios will become much more aggressive (almost on par with the current parallel shocks). Those types of shocks may become binding for banks that actively take positions along the yield curve, managing exposures by balancing sensitivities across different maturities. The revised SOT would then put the spotlight on vulnerabilities that were generally understated under the prior methodology.

Recommended next steps

The Basel Committee targets implementation by 1 January 2026, though regional timelines remain uncertain. The EBA has yet to issue a final proposal to transpose the framework into EU law, while the UK PRA intends to adopt the revised SOT from July 2026.

Until there is more clarity on the timeline, banks should prepare for early compliance and anticipate the impacts by comparing the SOT results under the old and new calibrations and analysing required adjustments to their limit frameworks and hedging strategy. As mentioned previously, this is particularly relevant for institutions with large portfolios of fixed-rate loans originated at high interest rates and/or those sensitive to non-parallel shocks given the potentially disproportionate impact the recalibration may have on their IRRBB risk profiles.

Institutions should also strengthen governance and reporting frameworks to meet enhanced requirements. Close coordination between Treasury, ALM, and Risk functions will be critical to ensure consistent assumptions and interpretations across management, reporting and disclosure.

Given the uncertainty around EU and UK implementation dates, banks should assume the recalibrated framework will effectively serve as the supervisory benchmark from 2026. Early preparation will support compliance and enhance strategic flexibility in managing structural interest rate risk.